Top-Down Analytics (TDA) is a management consulting firm specialising in analytical technologies that provides decision-making information to the leaders of scientific technology companies. TDA has published its report on the mass spectrometry (MS) market which contains a user survey and discusses the market conditions at the end of 2023.

Thank you to Glenn Cudiamat and TDA for conducting this informative market research and for allowing us to report on the results. This blog will give an overview of TDA’s results from the past year, looking at each technology classification in greater detail.

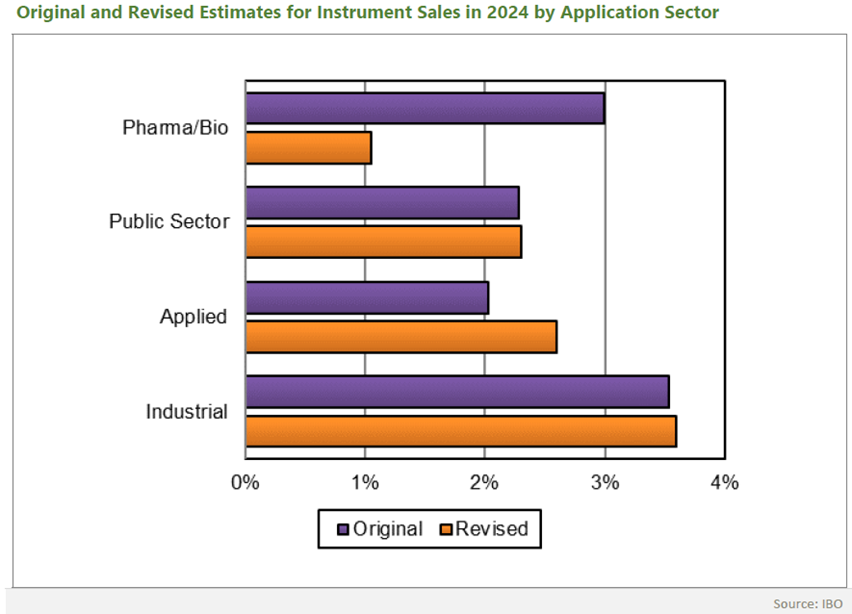

The overall MS market outlook

The total size of the MS market is $4.7 billion with a compound annual growth rate (CAGR) of mid-single digits through 2028. The market increase will be fuelled by demand for high resolution (HR) and ultra-high resolution (UHR) MS systems.

The largest regional market is Asia, driven by demand in China. Although gains in the Chinese market is expected to slow over this time period, it will be offset by increased demand from India. The pharma/biopharma industry accounts for 41 percent of the market and is expected to grow to $2.6 billion by 2028.

Future demand

Looking ahead, the growth of the MS market will be driven by increased demand for UHR technologies, with North American customers accounting for about a third of this. This expansion will be led by life science and pharma/biopharma, fuelled by demand for biotherapeutic research.

The TQ LC/MS market is expected to increase by mid-single digits, again, fuelled by pharma/bio and clinical applications accounting for over half of the market. The SQ LC/MS market is expected to expand by mid-single digits annually, driven by demand from the pharma/bio and environ/food industries – making up over three fifths of the market.

SQ GC/MS systems are the workhorse of the market, accounting for about 70 percent of the total; however, demand for TQ instruments is expected to drive overall GC/MS market growth. The environmental/food end market and the public sector together are expected to make up about three-quarters of the GC/MS market as testing of pollutants and pesticides continues to drive demand.

Survey demographics

The survey has 112 participants, representing nine end markets classified into pharma/biopharma, public sector, industrial, environmental and food, and applied/other. Over half of the respondents are from pharma/biopharma or contract research organisation (CRO) labs. As for their lab function, almost one third of respondents are from basic research labs, with another third from analytical services. The majority of the respondents’ job roles are supervisor/group lead, lab manager or director, in organisations with 2,001-10,000 full-time employees.

Usage and vendor familiarity

- The most common MS systems among respondents' labs are triple quad (TQ) liquid chromatography (LC)/MS and single quad (SQ) LC/MS, with more than half of the pharma/biopharma respondents’ labs using SQ LC/MS systems

- One-third of all respondents' laboratories employ targeted proteomics, protein structure analysis, and bottom-up proteomics/protein ID workflows

- Ease of maintenance and ease of use are the factors most likely to influence the respondents’ MS purchase decisions.

HR/UHR MS

- About two-thirds of respondents report having up to three active HR/UHR MS systems in their labs that are no more than seven years old

- Two-fifths report using their HR/UHR MS instruments daily and many run up to 100 samples per week.

TQ LC/MS

- Half of the respondents state that their labs own up to three active TQ LC/MS systems which are less than four years old

- Two-fifths of the respondents report using their TQ LC/MS instruments daily and that they run up to 100 samples each week

- Software and sensitivity are the most frequently identified areas for improvement for TQ LC/MS systems.

SQ LC/MS

- More than half of all respondents have more than four active SQ LC/MS systems in their labs and one-third indicate that their labs’ most active SQ LC/MS systems are no more than seven years old

- Two-thirds report using their SQ LC/MS instruments no more than a few times per week and most respondents run fewer than 25 samples per week

- Sensitivity and MS software are among the few suggestions for improvement for SQ LC/MS instruments.

Gas chromatography (GC)/MS

- 50 percent of respondents report having more than four active GC/MS instruments in their labs and around the same number indicate that their labs’ most active systems are at least eight years old

- Around two-thirds state they use their GC/MS instruments no fewer than a few times per week and most run fewer than 25 samples per week

- Software and service are among the suggestions for improvement for GC/MS systems.

TDA supports leaders in the scientific technology industry in identifying market opportunities through the provision of quantitative and qualitative survey solutions. They publish an annual industry report which can be accessed here. For more information on how they can help your business visit their website.

The report is available from TDA for $9000, please contact us directly. The Scott Partnership specialises in supporting scientific technology businesses navigate the intricacies of both local and international markets. Our extensive 20 years’ experience in the mass spectrometry market enables us to provide tailored solutions that directly address your specific goals. If you’re looking for support in the MS market or for industry specific events such as ASMS, please contact us directly at business@scottpr.com.